TL;DR:

- Financial advisors must ensure their social media content complies with SEC and FINRA regulations to avoid penalties. Building operational systems for content approval, recordkeeping, and supervision is essential for maintaining compliance and supporting growth. Automated workflows and proper training help ensure ongoing regulatory adherence across all platforms.

Compliant social media use for financial advisors is defined as publishing, archiving, and supervising digital content in full alignment with SEC Rule 206(4)-1 and FINRA Rule 2210. These two frameworks govern everything from a LinkedIn post about market performance to a client testimonial on Instagram. Get either wrong and you face enforcement action, fines, or reputational damage. Get them right and social media becomes one of the most cost-effective growth channels available to your practice. This article breaks down the regulations, the workflows, and the operational controls you need to use social media compliantly as an advisor in 2026.

What are the key regulatory frameworks for social media compliance?

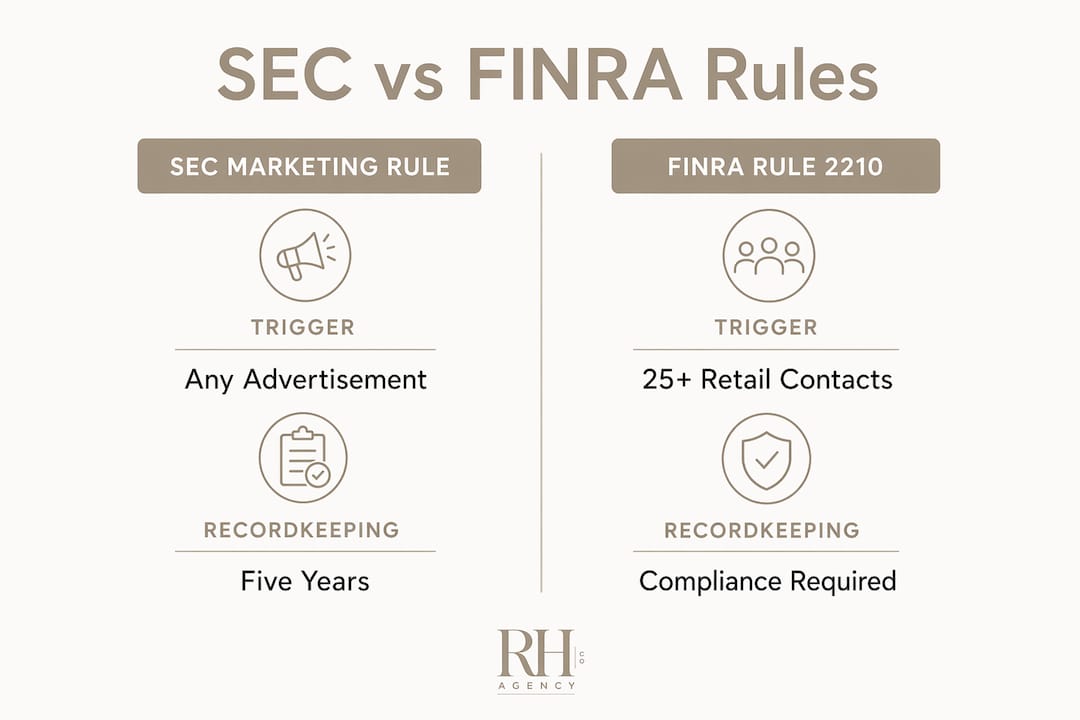

Two rules define the compliance floor for advisor social media: the SEC Marketing Rule and FINRA Rule 2210.

The SEC Marketing Rule, formally Rule 206(4)-1 under the Investment Advisers Act, treats social media posts as advertisements subject to substantiation and retention obligations. That means every post promoting your services, sharing performance data, or featuring a client story must meet the same standards as a formal brochure or email campaign. The rule applies to all SEC-registered investment advisers regardless of firm size.

FINRA Rule 2210 adds a distribution-based trigger. Retail communication requirements activate when content reaches more than 25 retail investors within 30 days, requiring principal approval and retention. That threshold is easier to hit than most advisors realize. A single LinkedIn post shared by colleagues can cross it within hours.

How SEC and FINRA rules overlap for dual-registered advisors

Dual-registered advisors, those holding both RIA and broker-dealer registrations, must satisfy both frameworks simultaneously. The SEC rule focuses on content accuracy and substantiation. The FINRA rule focuses on distribution volume and approval workflows. The table below shows where the rules diverge.

| Requirement | SEC Marketing Rule | FINRA Rule 2210 |

|---|---|---|

| Trigger | Any advertisement or promotion | Distribution to 25+ retail investors in 30 days |

| Approval | Compliance review before publication | Principal pre-approval for retail communications |

| Retention | 5 years, first 2 readily accessible | 3 years minimum |

| Scope | All SEC-registered advisers | FINRA member firms and registered reps |

Understanding which rule applies, and when both apply, is the starting point for any compliant social media strategy.

How to build social media policies and approval workflows

A written policy is not enough. Policies must be operationalized through daily supervisory controls that can be verified during an SEC or FINRA exam. Here is how to build a system that holds up.

- Define who can post. Specify which employees and advisors are authorized to publish on behalf of the firm. Personal profiles used for business purposes fall under the same rules as official firm accounts.

- Create content risk tiers. Tier 1 content, such as general educational posts, may require only a compliance review. Tier 2 content, including performance claims or testimonials, requires principal pre-approval before publication.

- Implement a pre-approval workflow. Use compliance platforms like Smarsh, Global Relay, or Hearsay Social to route draft posts through approval queues. These tools timestamp approvals and create an audit trail.

- Train advisors regularly. Annual training is the minimum. Quarterly refreshers tied to enforcement updates are better. Training records should be retained as part of your compliance documentation.

- Test your controls. Run periodic spot checks on published content to confirm that posts match approved drafts and that no unauthorized content has gone live.

Pro Tip: Build a content calendar with compliance checkpoints built in. When marketing and compliance teams share the same calendar, approval bottlenecks shrink and advisors spend less time waiting for sign-off.

Workflow automation and tiered approval systems are critical for managing the speed and volume of social media without creating compliance gaps. Manual review alone does not scale.

What recordkeeping practices are mandatory for social media?

Recordkeeping is where many firms fail during exams. The SEC requires 5-year retention of advertisements, with the first two years kept readily accessible. Social media posts are advertisements. That means every post, edit, and deletion must be captured and stored.

Effective archiving goes beyond saving a screenshot. Compliance teams should treat each post as a version-controlled unit, preserving the exact content as it appeared to users at the time of publication, including any edits made after posting. Deletions must also be logged, not simply removed from the record.

Supporting documentation is equally mandatory. Required files include:

- Copies or screenshots of the post as published across each platform

- Disclosure text shown to users at the time of viewing

- Performance worksheets and source data supporting any return figures

- Endorsement agreements and conflict-of-interest disclosures for testimonial content

| Documentation Type | Purpose | Retention Period |

|---|---|---|

| Post screenshots | Reconstruct content as published | 5 years |

| Disclosure text | Verify prominence and clarity | 5 years |

| Performance worksheets | Substantiate return claims | 5 years |

| Endorsement agreements | Confirm compensation disclosures | 5 years |

Archiving platforms like Smarsh and Global Relay integrate directly with LinkedIn, Twitter/X, Facebook, and Instagram to capture content in real time. Relying on manual exports creates gaps that examiners will find.

What are best practices for testimonial and endorsement compliance?

The SEC Marketing Rule permits testimonials and endorsements, but the compliance requirements are specific. Common enforcement failures involve missing or unclear disclosures about client status, compensation arrangements, and conflicts of interest. The problem is almost never the absence of a disclosure document. The problem is placement and clarity within the post itself.

The SEC requires disclosures to be clear and prominent within the social media post, not buried in a linked page or hidden below a "see more" fold. For short-form platforms like Instagram or X, this creates a real formatting challenge that requires deliberate planning.

Practical steps for testimonial compliance:

- Link each endorsement to a substantiation file that includes the endorsement agreement, compensation details, and any conflict disclosures before the post goes live.

- Place disclosures in the first visible lines of the post, not at the end after a "read more" break.

- Review influencer and referral program content under the same standards as direct client testimonials. Paid referrals are endorsements under the rule.

- Document the review process for each testimonial post so examiners can trace approval from draft to publication.

Pro Tip: Create a testimonial compliance checklist that lives inside your content approval workflow. Every testimonial post should clear the checklist before it enters the approval queue, not after.

How to monitor and supervise social media compliance daily

Ongoing supervision is the operational layer that keeps your compliance program functional between exams. FINRA's retail communication rule applies to both organic and paid social posts, which means compliance teams must track distribution reach by channel and post type, not just by content category.

A practical supervision framework includes four steps:

- Map your platforms. Document each social channel in use, whether it is a company page, personal profile, or paid ad account, and assign a distribution measurement method to each.

- Monitor third-party comments. Client comments on firm posts can create implied endorsements or contain misleading claims. Establish a response protocol that addresses complaints without creating new compliance exposure.

- Track distribution thresholds. Use analytics tools to measure reach per post within 30-day windows. When a post approaches the FINRA 25-investor threshold, trigger the retail communication review workflow.

- Conduct routine supervisory reviews. Assign a principal to review published content monthly and document findings. Adjust policies when patterns of non-compliance appear.

Compliance must be a living process with controls verified during exams, not just a written policy. SEC staff guidance makes clear that operationalized controls, not documentation alone, define a compliant program.

Adapting your supervision program to regulatory updates is not optional. The SEC and FINRA both issue guidance and enforcement releases that signal where examiners are focusing. Assign someone to monitor those releases and translate them into policy updates within 30 days of publication.

Key takeaways

Financial advisors who use social media compliantly must build governance, recordkeeping, and disclosure controls that satisfy both SEC Rule 206(4)-1 and FINRA Rule 2210 simultaneously.

| Point | Details |

|---|---|

| Know your regulatory triggers | SEC covers all adviser posts; FINRA Rule 2210 activates at 25+ retail investors in 30 days. |

| Operationalize your policies | Written policies without daily supervisory controls will not survive an exam. |

| Archive every version | Capture posts, edits, deletions, and substantiation files for a minimum of 5 years. |

| Place disclosures prominently | Testimonial disclosures must appear in the post itself, not on a linked page. |

| Automate distribution tracking | Use compliance platforms to measure reach and trigger the right approval workflow per channel. |

The compliance bottleneck nobody talks about

Most advisors I work with understand the rules well enough. What they underestimate is the operational weight of executing compliance every single day across multiple platforms, multiple advisors, and multiple content types. That gap between knowing the rule and running the process is where violations actually happen.

The advisors who handle this well are not necessarily the ones with the biggest compliance teams. They are the ones who have built systems. They delegate content calendar management to a trained support professional. They use archiving platforms that capture posts automatically rather than relying on someone to remember to take a screenshot. They treat the approval workflow as a production pipeline, not an afterthought.

What I have seen work consistently is pairing a compliance officer's regulatory knowledge with an operational support layer that handles the logistics. The compliance officer sets the rules. The support team runs the checklist, routes the approvals, files the documentation, and flags anything that needs a second look. That division of labor is what makes compliant social media sustainable at scale.

The advisors who struggle are the ones trying to do all of it themselves, or the ones who assume a policy document is the same as a functioning program. It is not. The advisor growth consulting conversation always comes back to the same point: growth requires systems, and compliance is no different.

— Jessica

How the right hand agency co supports advisor compliance operations

Financial advisors need more than regulatory knowledge to stay compliant on social media. They need operational infrastructure that runs consistently without adding hours to their week.

The Right Hand Agency Co provides operational support for financial advisors and RIAs, including marketing coordination with compliance oversight, content calendar management, approval workflow setup, and archiving system integration. Our executive assistants handle the day-to-day logistics of content routing, documentation filing, and platform monitoring so your compliance officer can focus on judgment calls rather than administrative tasks. We also support technology and systems integration for compliance platforms like Smarsh and Global Relay. If your social media compliance program needs an operational backbone, we build it.

FAQ

What social media posts require SEC compliance review?

All posts by SEC-registered advisers that promote services, share performance data, or feature client experiences are treated as advertisements under Rule 206(4)-1 and require substantiation and retention.

When does FINRA rule 2210 apply to social media?

FINRA Rule 2210 applies when social media content reaches more than 25 retail investors within 30 days, triggering principal approval and retention requirements regardless of whether the post is organic or paid.

How long must advisors retain social media records?

The SEC Marketing Rule requires a minimum 5-year retention period, with the first 2 years kept readily accessible. Records must include the post as published, any edits, and all supporting substantiation files.

Where must testimonial disclosures appear on social media?

Disclosures must be clear and prominent within the post itself. Placing them on a separate linked page or below a content fold does not satisfy SEC requirements and is a common enforcement failure.

Can a personal LinkedIn profile create compliance exposure for an advisor?

Yes. Personal profiles used to promote advisory services or share firm-related content fall under the same SEC and FINRA rules as official firm accounts and must be included in the firm's supervisory program.